ARS: Annual report to security holders

Published on April 20, 2006

Contents

| Financial Highlights | 1 | |||||

| Company Overview | 1 | |||||

| Letter to Shareholders | 3 | |||||

| Reinsurance | 8 | |||||

| Ventures | 12 | |||||

| Individual Risk | 14 | |||||

| Finance and Administration | 17 | |||||

| Underwriting Tools for the 21st Century | 19 | |||||

| Board of Directors | 23 | |||||

| Senior Officers | 23 | |||||

| Comments on Regulation G | 24 | |||||

| Form 10-K | 26 | |||||

| Corporate Information | Inside Back Cover | |||||

Financial Highlights

RenaissanceRe Holdings Ltd. and Subsidiaries

| Operating

(Loss) Earnings Per Share* |

Tangible Book

Value Per Share Plus Accumulated Dividends* |

Operating Return on Common Equity* |

||||||||

|

|

|

||||||||

| (In thousands, except per share data) | 2005 | 2004 | 2003 | 2002 | 2001 | |||||||||||||||||

| Gross premiums written | $ | 1,809,128 | $ | 1,544,157 | $ | 1,382,209 | $ | 1,173,049 | $ | 501,321 | ||||||||||||

| Operating (loss) income available to common shareholders* | (274,451 | ) | 109,666 | 525,488 | 341,889 | 166,860 | ||||||||||||||||

| Net (loss) income available to common shareholders | (281,413 | ) | 133,108 | 605,992 | 342,879 | 184,956 | ||||||||||||||||

| Per Common Share Amounts | ||||||||||||||||||||||

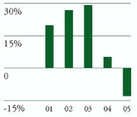

| Operating (loss) income* – diluted | $ | (3.89 | ) | $ | 1.53 | $ | 7.40 | $ | 4.87 | $ | 2.67 | |||||||||||

| Net (loss) income – diluted | (3.99 | ) | 1.85 | 8.53 | 4.88 | 2.96 | ||||||||||||||||

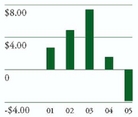

| Book value | 24.52 | 30.19 | 29.61 | 21.37 | 16.14 | |||||||||||||||||

| Dividends declared | 0.80 | 0.76 | 0.60 | 0.57 | 0.53 | |||||||||||||||||

| Operating ratios | ||||||||||||||||||||||

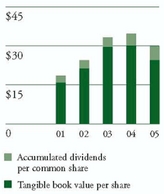

| Operating return on average common equity* | (13.3 | %) | 5.1 | % | 29.3 | % | 26.9 | % | 19.9 | % | ||||||||||||

| Net claims and claim expense ratio | 116.6 | % | 81.9 | % | 33.0 | % | 41.2 | % | 38.8 | % | ||||||||||||

| Underwriting expense ratio | 23.1 | % | 22.5 | % | 23.4 | % | 19.0 | % | 25.4 | % | ||||||||||||

| Combined ratio | 139.7 | % | 104.4 | % | 56.4 | % | 60.2 | % | 64.2 | % | ||||||||||||

| * | In this annual report we refer to various non-GAAP measures, which are explained in the Comments on Regulation G on page 17. |

Company Overview

RenaissanceRe was established in June 1993 to write property catastrophe reinsurance. By pioneering the use of sophisticated computer models to construct our portfolio, we have become one of the world’s largest and most successful catastrophe reinsurers. We have leveraged our expertise to establish leading franchises in additional selected areas of insurance and reinsurance where we believe we can enjoy a competitive advantage.

1

Today, we provide Catastrophe Reinsurance and Specialty Reinsurance. Additionally, we manage joint ventures which provide Catastrophe Reinsurance and Specialty Reinsurance, and we opportunistically invest in strategic joint ventures. We also write primary insurance and quota share reinsurance through our Individual Risk unit.

2

Letter to Shareholders

RenaissanceRe remains committed to the strategy upon which it was founded — disciplined risk-taking and opportunistic entry into markets, supported by sophisticated risk-management technology, prudent capital management and exceptional client service.

Last year was the worst year in our company’s 13-year history. We reported our first-ever annual operating loss, losing $274 million as a result of an unprecedented level of hurricane activity in the Southern U.S., and experienced the loss of members of our senior management team in connection with the investigations into the company’s restatement of its financial results. But RenaissanceRe is a resilient company, combining financial strength with experienced professional talent. Our employees have performed well by smoothly handling the management transition and at the same time executing effectively in operating our business.

A High Catastrophe Year

We estimate that industry insured losses for the 2005 hurricanes will exceed $80 billion, making it the most costly on record. Although some people in our industry did not seriously imagine the likelihood of so damaging a series of storms, or believed such things might occur only once in a hundred years, according to our models we estimate that the industry should expect this magnitude of worldwide annual aggregate losses to occur on average once every fifteen to twenty years. Though the impact of this level of industry losses will vary for an individual company depending on the concentrations of its book of business and the nature of the events that have occurred, the level of losses incurred in 2005 should not have been outside the range of modeled expectations.

Given this expectation, we were prepared to handle the 2005 hurricanes and are proud we responded so well, paying claims quickly and continuing to be a lead market for catastrophe reinsurance. This confirmed our role as an industry leader, and was appreciated by our clients.

Nevertheless, the hurricanes took their toll: Katrina caused a net negative impact of $443 million, and Wilma had a net negative impact of $314 million. The total impact of the 2005 hurricanes in the third and fourth quarters was $909 million, or about 1% of our estimate of total industry insured losses for these events. As a result, our operating loss was $274 million for the year, and our operating loss per share was $3.89. Book value per share fell by approximately 19%, to $24.52.

It is important to appreciate that our share of industry losses differed significantly for the two major storms. For Katrina our loss was roughly 0.7% of our estimate of $60 billion of industry losses, and for Wilma our loss was roughly 2% of our estimate of industry losses of $15 billion. These outcomes reflect our decision to be underweight for many of the classes of business that were heavily affected by Katrina such as offshore energy, commercial property and property per risk coverage. For these lines, we believed the catastrophic loss potential was underestimated and as a result the pricing was inadequate, so we did not write much of this business. We also continue to believe that it is inherently more difficult to model the potential damage to commercial property than to residential property, and so maintain relatively limited exposure to commercial portfolios. While the same underwriting approach applied to Wilma, we experienced a larger relative loss for this event driven by our decision to be overweight in Florida where we viewed the pricing as attractive.

Still, this past year’s losses, following on the heels of a high-catastrophe year in 2004, might lead you to question how well our statistical models function, and even whether we should be in the catastrophe reinsurance business altogether. We ask ourselves similar questions. It is part of our risk management culture to continually test our models and our approach, and not just in the aftermath of a major catastrophic event. We do so to evaluate our underwriting decisions and also to evaluate the analytical tools we use to make those decisions. This is part of an overall goal to continually refine and improve the way we manage risk. Our proprietary REMS© modeling system is fundamental to our underwriting practice and philosophy, and we have devoted considerable resources and intellectual capital to this technology.

Consistent with this goal, following the 2005 hurricane season, we completed a comprehensive review of our North Atlantic hurricane model. This was the conclusion of work we initiated following

3

the 2004 hurricane season. Drawing upon a large pool of talent throughout our organization — including meteorologists, climatologists, statisticians and underwriters — we undertook an intensive reexamination of scientific and industry data and concluded that we have entered a period of higher frequency and severity of North Atlantic hurricanes. Given that our prior models, like most commercially available models, were calibrated to long-term historical averages, we increased the frequency assumptions in our REMS© model in November of 2005 and have been underwriting with this model since then. We believe we were the first reinsurance company to fully integrate revised frequency assumptions into its models for North Atlantic hurricanes. The vendor models, which most of our competitors use, are not expected to be updated until the second quarter of 2006. This gave our underwriters an analytical advantage at the January 1st renewals in 2006, which allowed us to get better access to the business we wanted to write, and we believe that for 2006 we have constructed a book of business that is better than 2005’s, in part due to higher rates for catastrophe reinsurance in the post-Katrina market.

This interest and effort to better understand the peril of hurricanes is not something new at RenaissanceRe. Our commitment to research into the area of catastrophic risk has been in place for more than a decade. We have worked independently and with peers in our industry to fund innovative research on catastrophic perils. We have used the results from this research to improve our models and educate ourselves and our clients about ways to manage and mitigate the impact of natural catastrophes. For example, last year we funded a facility called the ‘‘RenaissanceRe Wall of Wind’’ at the International Hurricane Research Center at Florida International University, which is designed to test wind loads on various structures to help structural engineers design buildings that are more wind-resistant. We hope these efforts will contribute to mitigating damage from future hurricanes, which will benefit both our clients and us.

As to whether we should remain in the catastrophe business, we continue to believe that over time this business can produce attractive returns, if pursued with prudent risk selection and careful underwriting — concepts that are fundamental to our company’s culture. We recognize that our business requires us to assume significant risk, but we do our best to make sure these risks are well understood, well defined, and that we are appropriately compensated for assuming them.

There is a tendency in our business to over-steer following large catastrophe losses and underwrite against the prior year’s events. While assumptions need to be tested against actual results, the data we use to calibrate our models is more robust than the underwriting outcome of a single year. Given the relatively low frequency of catastrophic events, underwriters in our industry can sometimes be lulled into a false sense of complacency by recent results and will often end up under-pricing business in regions where losses have been light. We are disciplined in our approach and seek to avoid under-priced business. Over the long-run we expect this discipline to translate into superior results. Our track record indicates we have done a good job; over the last ten years we have grown tangible book value plus accumulated dividends at close to 17% per year.

4

While we remain committed to writing catastrophe reinsurance, we continue to look for opportunities to diversify our business into additional areas where we can apply our expertise. During the year, our Individual Risk segment grew 36% and accounted for 35% of our gross managed premium. In addition, our Specialty Reinsurance business continues to develop well-received franchises in attractive niche areas, taking advantage of market opportunities, although we expect premium volume to be down in 2006 due to the loss of a few large contracts, higher retentions, and fewer interesting opportunities at year end than we had anticipated.

Operations Unaffected during Management Changes

During the year, Jim Stanard, the company’s co-founder, resigned as Chairman and Chief Executive Officer, and the two of us, Neill Currie and Jim MacGinnitie, together assumed his duties. Neill, who had co-founded RenaissanceRe with Jim Stanard in 1993 and had returned to the company during 2005, assumed the position of Chief Executive Officer. Jim MacGinnitie, who had served on the Board since 2001, stepped up to become non-executive Chairman.

Other management changes included the appointment of Bill Riker as Chief Underwriting Officer for the company. Bill, who has for years been a major force at RenaissanceRe and instrumental in developing our proprietary technology, had been head of our Individual Risk business. Bill Ashley, who has worked closely with him, moved up to assume Bill’s responsibilities in Individual Risk. Kevin O’Donnell, who has been in charge of our Catastrophe Reinsurance operations, was given expanded duties to head our entire reinsurance subsidiary, including oversight of Specialty Reinsurance, which had previously been led by Michael Cash. In addition, John Lummis, our Chief Operating Officer and Chief Financial Officer, has indicated that he intends to leave the company at the end of his contract term in June 2006.

We are pleased that the transitions made to date have been smooth and efficient. Our core operating engine has functioned without interruption. The methodologies and key concepts upon which this company was founded have been institutionalized and rooted throughout the organization. Today, RenaissanceRe has grown to be a company of almost 200 people, with operations in Bermuda,

5

Dallas, Raleigh and Dublin. Our people are motivated and proud to be part of an industry leader. They value the intellectual and technological resources available at RenaissanceRe, which make working at our company professionally rewarding.

During the past year, we also focused on further nurturing our professional talent. We initiated our Leadership Development Institute, a management development program to further cultivate our senior personnel. As part of this program, we bring in leaders and thinkers from outside the organization for lectures, workshops and coaching, to help our people develop their skills and harness their talents. As we grow, we seek to create not just an intellectually vibrant atmosphere, but also a mature and sustainable franchise.

We also had cause to be proud of our employees as they worked together to serve our clients and other stakeholders in the midst of the regulatory challenges and executive transitions we faced last year. We will continue to focus on strong accounting, compliance and internal audit functions, and will look to bolster our staff, processes and other resources in these areas. Perhaps even more importantly, we have reinforced that our company's strength is drawn from a culture of honesty, transparency, and ethical business practices, and we will seek to ensure that every member of our team will uphold the highest standards. We will continue to cooperate fully with the ongoing regulatory and government investigations and will make every effort to put these matters behind our company.

Looking Ahead

The past year was difficult, but we look to the future with optimism. We believe that opportunities within the marketplace, especially in our core catastrophe business, should continue to be strong, and we have so far constructed an attractive portfolio of business for the year ahead. Southeast U.S. catastrophe risk continues to represent an area of peak demand with constrained supply, and so we expect pricing to remain attractive. However, other geographic areas and perils have not adjusted for the lessons of 2005, and there are still many programs that are inadequately priced in our view. Aside from catastrophe-exposed business, market conditions are inconsistent, with little evidence of broad price firming like we saw in 2002.

6

In approaching these market conditions, we expect to bring the same philosophy that we always have: we will focus on the interests of the long-term shareholder, challenge ourselves to think carefully about the risks we are taking and seek to write only business that is attractively priced. For any business that we are in, that may mean growing or shrinking our premiums in any given year — and this may prove disappointing relative to others’ expectations. Importantly, RenaissanceRe remains committed to the strategy and philosophy it was founded upon: careful and disciplined risk selection, opportunistic entry into markets experiencing dislocation or sudden change, leadership in the use of information and technology, prudent capital management and exceptional client service. These tenets have served our company and its shareholders well, and should continue to do so in the future.

Sincerely,

Neill

A. Currie

Chief Executive

Officer

W.

James MacGinnitie

Chairman of the

Board

7

Reinsurance

Catastrophe Reinsurance

The combination of hurricanes Katrina, Rita and Wilma delivered an enormous hit to the industry and to our own reinsurance business, which experienced a net negative impact from these storms of $760 million. Our balance sheet was strong so that it could absorb these losses and support our business going forward.

As in other active hurricane seasons, we served our clients in 2005 by being well-positioned to understand the magnitude of their losses and the implications of these losses on their businesses. We provided additional coverage to many of our customers through back-up and live cat reinsurance to protect them as storms exhausted their coverage. Although the underwriting approach for these products is quite different from normal catastrophe reinsurance, we have developed sophisticated tools and draw upon internal resources in order to price this risk with precision.

Looking ahead, we see improved market conditions for many parts of our U.S. business. Markets that had been softening before Katrina have turned around, and U.S. clients have seen their premiums increase substantially. We expect to continue to participate in the Florida market, despite the hurricanes, but will seek to manage our exposure carefully. Of all the major catastrophe-insured geographic areas, in our estimation Florida still offers the highest risk-adjusted returns over time.

We are also seeing opportunities to write attractively priced retrocessional business, which is reinsurance for other reinsurance companies. Due to concerns about both pricing and terms, we had significantly reduced our writings in this market in 2005. This market sustained significant losses in 2005, and pricing and terms improved meaningfully for January 1, 2006 renewals. We believe that we bring unique underwriting tools to this difficult market and are well-positioned to outperform in this sector in the future (as we have in the past).

Specialty Reinsurance

Specialty Reinsurance contributed positively to our 2005 results, though this was driven by the reduction in our Specialty reserves following our third quarter loss reserve review. Premiums were about flat in 2005 versus 2004 as the market itself was generally stable.

For 2006, we expect a decline in our written premiums. We have lost several large contracts due to customer-specific issues — a client was acquired and others decided to retain more risk — and the impact of the 2005 hurricanes has not driven prices or terms for many lines of business to levels that we find attractive.

Our strategy remains consistent: we are focusing on a relatively small number of transactions in a small number of specialties where we seek to understand the risk we are assuming and be appropriately compensated. We are now a well-established reinsurer for workers’ compensation catastrophe, terrorism, casualty clash and surety. During 2005, we enhanced the underwriting models we use for workers’ compensation and terrorism, and we increased the rigor of our casualty clash underwriting, where we believe we are now recognized as a market leader.

8

Disciplined Underwriting

Across both areas of our reinsurance business, underwriting discipline will be critical. Many new participants have entered the market, and it is too early to determine what their effect will be. We will not seek market share and will refrain from writing business that we do not think is adequately priced. The markets we operate in are inefficient, but our underwriters understand our risk metrics and seek to exploit inefficiencies by taking a greater share of the best business. We understand the effects of diversification and will, of course, strive to optimize our portfolio, but we will accept being overweight in certain risks so long as we believe we are being appropriately paid to take these risks. This means we will underperform in some scenarios, but in the long run we believe this will result in superior returns.

9

10

11

Ventures

RenaissanceRe’s Ventures unit is a distinguishing feature of our company. Through it, we engage in three key activities: developing and managing joint ventures, identifying and making strategic investments, and creating customized reinsurance products. Our joint ventures enable us to leverage our underwriting expertise and allow partners to invest and participate alongside us. RenaissanceRe manages the joint ventures’ business, earning fees in addition to our share of profits for the investments we have made in these deals. We also make strategic investments in entities managed by well-regarded firms, from whom we feel we can profit while learning. In customized reinsurance, we design structures that allow counterparties to participate in the underwriting results of portions of our business, generating fees and commissions for RenaissanceRe and shaping our retained portfolio. Our Ventures group manages all three of these activities and is dedicated to structuring the deals and managing the relationships by serving as a bridge between RenaissanceRe and our partners and investors.

Our largest joint ventures, DaVinci Re (established in 2001) and Top Layer Re (established in 1999), have their own balance sheets and participate in catastrophe risks that are evaluated by RenaissanceRe. In 2005, as with RenaissanceRe, DaVinci experienced significant hurricane losses. In anticipation of attractive market conditions for 2006, we succeeded in restoring and expanding DaVinci’s capital base by raising $325 million from new and existing third-party investors eager to take advantage of the impending opportunity in property catastrophe reinsurance. RenaissanceRe continues to hold a sizeable equity interest in DaVinci, though it has been reduced to 20% with the additional capital.

Top Layer Re, in which we hold a 50% interest, participates in catastrophe program layers that are ‘‘higher’’ (more remote) than those assumed by RenaissanceRe or DaVinci. It also writes exclusively outside the U.S. Once again, Top Layer experienced a loss-free year, its record unbroken since its inception. While market conditions have improved in the U.S., they have softened in other parts of the world. Consistent with our commitment to underwriting discipline, Top Layer did not renew several programs. If the hard market for hurricane-exposed business proves to have a beneficial ripple effect extending to Top Layer’s non-US territories, the balance of 2006 may see increased writings.

Prior to the onset of the hurricane season, we executed a few new, smaller strategic investments, in which clients sought capital in the wake of their 2004 hurricane losses to take advantage of market opportunities. As an example, the largest of these built upon our relationship with Tower Hill Insurance Group, one of our quota share partners. Through these investments, RenaissanceRe benefits from a return on our capital investment, from access to reinsurance business, and from payments for consultative services.

In early 2004, we made a strategic investment in Channel Re, a financial guaranty reinsurer, in partnership with MBIA, Koch Financial Corporation and Partner Re Ltd. Channel Re has now completed its second full year of operation with an attractive return, though slightly below our expectations. The business continued to be affected by the capital markets’ abundant availability of inexpensive capital and the investment community’s eagerness to reach for yield in a low-interest-rate environment. These conditions put pressure on pricing, and therefore on the volume, of primary financial guaranty insurance.

During 2005 we also sold our equity interest in Platinum Underwriters Holdings, Ltd. Although we maintain an ongoing consulting relationship with Platinum, helping to evaluate their catastrophe

12

book of business, and still hold Platinum warrants, we decided to dedicate this capital back into our core Reinsurance and Individual Risk businesses.

In reflecting on where we have come from, RenaissanceRe pioneered its joint venture strategy in 1999 with the formation of Top Layer Re. Recently, we have witnessed a proliferation of companies establishing or seeking to establish insurance and reinsurance vehicles similar to DaVinci, but we believe Top Layer and DaVinci remain differentiated in having a dedicated team of professionals managing the business, high credit ratings and the ability to write business directly for our customers. We believe this strategy expands our product capacity and product offering, and therefore our ability to better serve our customers and investors.

13

Individual Risk

The strong growth of our Individual Risk business represents a major success in achieving profitable diversification and building a strong franchise in areas of significant long-term opportunity.

RenaissanceRe’s Individual Risk business continued its strong growth in 2005, with a 36% increase in written premiums, to $651 million — up from a mere $50 million only four years ago. This represents a major success in our goal to bring profitable diversification to our company and build a strong franchise in areas where we see significant long-term opportunity.

Individual Risk operates under the banner of Glencoe Group Holdings Ltd. and receives business from three separate channels: from brokers, with whom we write business on a risk-by-risk basis; from program managers, with whom we partner on a small number of large transactions; and from clients, which are primary insurers for whom we provide quota share reinsurance. We seek to partner only with the highest quality firms that share our passion for data and the sophisticated use of risk modeling, and who understand our commitment to write business only for those risks that meet our stringent criteria for adequate return on capital. In the case of our program managers, we outsource to them tasks such as claims handling, marketing and back office processing, while we place our underwriters on site with them to provide oversight and ensure that our underwriting standards are carefully observed.

During 2005, our Individual Risk business was approximately evenly split between property and casualty insurance. Our catastrophe-related homeowners business once again was severely affected by the Florida hurricane season. We have established a position with key partners in the Florida market and anticipate that over the long term this will be a profitable book of business. Aside from that business, we were quite pleased with the performance of the rest of our portfolio.

One of the highlights of our year was our participation in three new programs, two of which were casualty-focused, and a third which writes agriculture-related property business. This brings to seven the number of programs in which we participate. Our program business is largely conducted at our Dallas operations, which have grown significantly over the past several years and to which we have attracted a talented team. We are now beginning to see the positive effects of leveraging this capability, and we are well positioned to take advantage of new opportunities.

In another development, this year we began to implement a new proprietary database and technology that we call our ‘‘PACeR’’ system, which we have developed over the past few years to track exposures in our casualty business and help with monitoring risk and underwriting. This complements our use of our REMS© system, which is the same tool used by our Reinsurance unit, to help with the analysis of catastrophe risk in our commercial property.

Looking ahead, the aftermath of Katrina resulted in considerable disruption in the commercial property market and we expect to be able to take advantage of select opportunities during 2006. Similarly, the catastrophe-exposed Florida homeowners reinsurance market should see meaningful price increases, which will increase our revenues, although we do not expect to pursue additional market share, given our current size in this market. Finally, we continue to examine new program possibilities and, in keeping with our strategy, look forward to adding a small number of large programs to that portion of our business.

14

15

16

Finance and Administration

Maintaining Capital Strength; Enhancing Infrastructure

While we are unhappy with the unprofitable results of 2005, the past year demonstrated the efficacy of our capital management. Notwithstanding record levels of catastrophe losses for our company and the industry, we successfully supported the capital needs of our business.

Sensible risk guidelines and rigorous risk management processes are part of the explanation for this. In addition, we had excess capital at our holding company that we contributed to recapitalize our operating subsidiaries following the losses in the third and fourth quarters of 2005.

Following the hurricanes, we took the following actions to supplement our capital resources and liquidity, and to position our company for 2006:

| • | We raised $325 million of equity capital for DaVinciRe Holdings Ltd. in December 2005 and February 2006 from third party investors to allow for growth of our core catastrophe reinsurance business and serve the needs of our customers. |

| • | The company drew down $150 million under its existing revolving credit facility to enhance the ability of the parent holding company to respond to unexpected needs. |

| • | We exited various investments to focus capital resources on our core business, including $114 million in net proceeds from the sale of our interest in Platinum Underwriters Holdings, Ltd. and $136 million of redemptions from various hedge funds. |

We also continued to develop our accounting systems over the past year. Most notably, we enhanced our processes for establishing and monitoring loss reserves and completed a loss reserve review for each area of our business according to our new processes. As a result of these reviews, we reduced our loss reserves by $249 million. However, while we have changed our reserving processes, we are maintaining a philosophy of prudent reserving.

Operational risk continues to be an area of focus as we develop an increasingly complex business model — with more products than ever — in an increasingly complex business environment. As an example, given its importance to our business model, we have worked to reinforce our technology infrastructure. In November, we completed an exercise to simulate the impact of a major disaster on our Bermuda operations in order to test our back-up systems: we were up and running off-site within three hours after the simulated event.

One key setback for the year was the one-notch downgrade that most of our operating companies received from each of the major rating agencies. The rating agencies took these actions in light of the departure of Jim Stanard as CEO, as well as our large hurricane losses. Fortunately, even after these

17

downgrades, our ratings continue to be among the highest in our industry peer group, and we did not perceive any meaningful impact to our business. Over time, we hope to see our ratings returned to former levels.

Solid Results from Investments

Our investment portfolio performed well in 2005, generating a total return of 3.7%, compared a return of 2.8% for the composite of our benchmark indices. Our returns benefited from our decision in June to take less interest rate risk and shorten the duration of our portfolio to 1.4 years.

We initiated several other changes to reduce the aggregate risk of our investment portfolio, including reducing our allocation to the high yield sector by 67% and reducing our investments in hedge funds by 55%. We did this in part because we believed we were not being adequately compensated for the risk we were taking, and also to enhance our liquidity given the hurricane losses. We will continue to monitor our strategy and whether to take on more risk in the investment portfolio in the future.

Credit Ratings

| S&P | A.M. Best | Moody’s | ||||||||||||

| Reinsurance Segment2 | ||||||||||||||

| Renaissance Reinsurance | A+ | A1 | A2 | |||||||||||

| DaVinci Re | A | A1 | — | |||||||||||

| Top Layer Re | AA | A+ | — | |||||||||||

| Renaissance Europe | — | A1 | — | |||||||||||

| Individual Risk Segment2 | ||||||||||||||

| Glencoe | — | A−1 | — | |||||||||||

| Stonington | — | A−1 | — | |||||||||||

| Stonington Lloyds | — | A−1 | — | |||||||||||

| Lantana | — | A−1 | — | |||||||||||

| Holding Company Senior Debt | A− | bbb1 | Baa1 | |||||||||||

| 1 | These ratings are under review, with negative implications |

| 2 | The A.M. Best, S&P and Moody’s ratings for the companies in the Reinsurance and Individual Risk segments reflect the insurer financial strength rating. |

18

Underwriting

Tools

for the 21st

Century

Most insurers and reinsurers now have the capability to incorporate off-the-shelf, vendor-derived probabilistic modeling into their underwriting processes, although there is a wide range in how extensively they use these models and their skills in employing them. At RenaissanceRe, we believe that the standard set of traditional vendor-supplied cat models, coupled with some basic actuarially based experience-rating tools, represents an increasingly inadequate approach to managing and controlling risk. As a result, in recent years we have pushed to ‘‘raise the bar’’ on our analytical tools as part of an ongoing process to improve our knowledge and to achieve a new underwriting paradigm.

1. Catastrophe Reinsurance Tools

In order to properly underwrite catastrophe risk, a reinsurer today should have underwriting tools that are greater in scope and flexibility than those generally available ‘‘off the shelf’’ from commercial vendors. The ability to supplement and modify these tools — for example, to use independent research for testing things like varying climatic scenarios — is now a requirement for any world-class catastrophe reinsurance underwriting organization.

In response to the occurrence of four major hurricanes hitting Florida in 2004 — and before the multiple hurricanes of 2005 — we extensively re-examined the historical data on hurricane frequency and climate signals. Although there still remains significant uncertainty, we came to the conclusion that we are now in an extended period of generally increased hurricane frequency and severity which we could not ignore in our pricing and risk management. As a result, starting in late 2004, using our revised models, we began stress-testing our portfolios to determine how they would perform under higher hurricane-frequency scenarios and to use these revised frequency assumptions in our pricing tools. In 2005, we continued to upgrade our understanding of the potential outcomes for increased hurricane frequency as well as for the overall frequency of severe storms. We incorporated these findings into our underwriting processes in the summer of 2005 and updated our models in November 2005.

19

This has maintained RenaissanceRe at the leading edge of the marketplace. As of yet, the commercial vendors have not updated their models and released their revisions to hurricane risk, and are not expected to do so until mid-2006. Reinsurers who rely primarily on commercial models are still waiting for these revisions in order to assess the changes affecting their underwriting decisions and their portfolios of insured risks.

Another important part of managing a portfolio of catastrophic risk is to create the most robust catalogue of potential catastrophic events that could occur. Commercially available models do not cover the full spectrum of perils and regions throughout the world. To create a more complete set of potential events, we need to supplement the events generated by the commercial vendors with our own statistically generated potential scenarios. These scenarios typically represent perils in less populous catastrophe-exposed areas, such as South African earthquake, or perils viewed as less serious, such as Australian hail, but over the years the industry has seen meaningful losses from these types of unmodeled perils.

2. Catastrophe-Exposed Individual Risk

Applying modeling technology to Individual Risk underwriting is an area where there have been many attempts, but few success stories. RenaissanceRe has developed tools, for use in our Individual Risk partners’ offices, to help our partners calculate the proper pricing for the catastrophe component of their individual insurance policies.

These tools combine our internally developed algorithms with the output of commercially available models, to provide information that can be used on a timely basis. Post-processing tools enable us to modify our pricing, to take into account changing climatic conditions and/or changing supply-and-demand dynamics in the marketplace.

The tools we have developed are applicable for both the personal lines homeowners market and the commercial lines business.

We deliver our personal lines products through a program we call TRAC (Theoretical Rate Adequacy Cube), which enables our clients to actively manage their portfolios for price adequacy and provides them with actionable steps to achieve their goals.

3. Other Pricing Tools for Non-Natural Peril

Catastrophe Risk

Tools to help measure and price catastrophe risk that falls outside the realm of traditional natural perils remain in their infancy. Most have emerged since the events of September 11, 2001. These tools, which we primarily employ in our Specialty Reinsurance business, are still very much in flux and so we have created our own tools to benchmark the vendor models and provide estimates in areas that the vendor models have not yet addressed. Our models include:

| • | Terrorism risk on both a conventional and NCB (nuclear/chemical/biological) basis; |

| • | Earthquake exposure in our workers’ compensation catastrophe book of business; |

| • | Incident exposure which also addresses cross-company correlations, in our workers’ compensation incident portfolio; |

| • | Fire per risk; and |

| • | Aviation. |

In addition, we have been working to develop tools that evaluate the correlations in our casualty clash portfolio, to better understand the unforeseen risks that exist when clients have multiple types of coverage that get triggered by the same loss incident.

20

4. Tools to Link and Reconcile Expected and Actual Outcomes

Another key piece of 21st century tools will be the ability to easily link and reconcile expected outcomes with actual outcomes. We believe that early detection of business signals is imperative.

At RenaissanceRe, we have developed our PACeR System, and have shared it with our program managers. This tool enables our underwriters and account executives to track the performance of their portfolios and sub-portfolios in real time, against their expected outcomes.

This is a considerable enhancement over traditional industry practice, in which a portfolio’s performance is calculated after the fact, by actuarial departments removed from the underwriter’s day-to-day business. By providing the information regarding loss-emergence at the underwriter’s fingertips, the underwriter can see how his portfolio is doing and fine-tune the writing of new policies to conform to new information.

These tools empower underwriters to make better decisions, by placing them closer to real-time data and equipping them with the complex actuarial mathematics needed for portfolio analysis and evaluation.

5. Business Intelligence Tools

Our newest area of concentration is on the development of business intelligence tools, and we believe it will be one of the most important over the next decade. Business intelligence tools provide a way to segment portfolios and derive non-intuitive insights into a portfolio’s underlying characteristics. This is a data-intensive process and requires a much higher level of data capture, due diligence and computational effort than has historically been the norm in the insurance business.

To date, business intelligence has provided us with some ‘‘low hanging fruit’’ in assessing our portfolio of risk. The ability to identify such low hanging fruit has been very beneficial, enabling us to take quick actions to capitalize on opportunities or make corrections. Over time, we expect this area will provide us with sustainable competitive advantages in the years to come.

Conclusion

The required tool set for a successful reinsurer today is much greater than it has been in the past. Companies that can develop and properly deploy these tools in the hands of their underwriters will have a competitive advantage over those companies that either lack the tools or at which the tools remain ensconced in the actuarial ivory tower.

The requirement to develop and deploy such tools will tend to increase the barriers to entry into the business (one of the few real barriers that exist in the reinsurance industry). Management

21

commitment to developing these tools, and professionals with the skill to use them, as well as the required intellectual curiosity, tend to be in very short supply. This has been reflected in the difficulty that many new companies have had in hiring the right people to implement the tools. Companies and investors must also be careful, as having the tools does not necessarily mean they are effective or are being effectively deployed.

Finally, having tools that can be deployed in real time by a company’s decision makers creates a tangible competitive advantage in that it enables underwriters to provide timely service to brokers and clients. Having decision makers who must make rough calculations in the heat of a negotiation is never an optimal situation.

22

| Board

of Directors

RenaissanceRe Holdings Ltd. |

Senior

Officers

RenaissanceRe Holdings Ltd. and Subsidiaries Effective April 1, 2006 |

|||||||||||||

| W.

James MacGinnitie

Chairman RenaissanceRe Holdings Ltd. Neill A. Currie Chief Executive Officer RenaissanceRe Holdings Ltd. Thomas A. Cooper TAC Associates Edmund B. Greene Retired General Electric Company Brian R. Hall Retired Johnson & Higgins Jean D. Hamilton Private Investor Independent Consultant William F. Hecht Chairman, President and CEO PPL Corporation Scott E. Pardee Alan R. Holmes Professor of Monetary Economics Middlebury College William I. Riker President RenaissanceRe Holdings Ltd. Nicholas L. Trivisonno Retired Chairman and CEO ACNielsen Corporation |

William J.

Ashley

Chief Executive Officer Glencoe Group Holdings Ltd. Jeffrey A. Aune Senior Vice President Glencoe U.S. Holdings Inc. Tracy H. Bowden Vice President General Counsel Glencoe U.S. Holdings Inc. Ian D. Branagan Senior Vice President Renaissance Reinsurance Ltd. Trevor A. Brooks Vice President RenaissanceRe Holdings Ltd. Neil A. Currie Chief Executive Officer RenaissanceRe Holdings Ltd. Ross A. Curtis Senior Vice President Renaissance Reinsurance Ltd. Peter C. Durhager Senior Vice President Chief Administrative Officer RenaissanceRe Holdings Ltd. Todd R. Fonner Senior Vice President Treasurer RenaissanceRe Holdings Ltd. Timothy J. Graff Senior Vice President Glencoe U.S. Holdings Inc. |

David A.

Heatherly

President Glencoe U.S. Holdings Inc. Jayant S. Khadilkar President Weather Predict LLC Robert J. Lamendola Senior Vice President Renaissance Reinsurance Ltd. James R. Lewis Vice President Renaissance Reinsurance Ltd. John M. Lummis Executive Vice President Chief Operating Officer and Chief Financial Officer RenaissanceRe Holdings Ltd. Sean M. Moore Vice President RenaissanceRe Holdings Ltd. John D. Nichols, Jr. Executive Vice President RenaissanceRe Holdings Ltd. Michael S. Nuenke Senior Vice President Glencoe U.S. Holdings Inc. Kevin J. O’Donnell President Renaissance Reinsurance Ltd. Justin O’Keefe Vice President Renaissance Reinsurance Ltd. Jonathan D. Paradine Senior Vice President Renaissance Reinsurance Ltd. |

Richard B.

Primerano

Senior Vice President Chief Financial Officer Glencoe U.S. Holdings Inc. Laurence B. Richardson II Vice President RenaissanceRe Ventures Ltd. William I. Riker President RenaissanceRe Holdings Ltd. Rebecca J. Roberts Vice President Renaissance Reinsurance Ltd. Apryle L. Satasi Vice President Renaissance Reinsurance Ltd. Brian C. Stahl Vice President Glencoe U.S. Holdings Inc. Craig W. Tillman President Wyndham Partners Consulting Ltd. Stephen H. Weinstein Senior Vice President Chief Compliance Officer General Counsel and Secretary RenaissanceRe Holdings Ltd. Mark A. Wilcox Senior Vice President Chief Accounting Officer Controller RenaissanceRe Holdings Ltd. |

|||||||||||

23

Comments on Regulation G

In addition to the financial measures set forth in this Annual Report prepared in accordance with accounting principles generally accepted in the Unites States (‘‘GAAP’’), the Company has included certain non-GAAP financial measures in this Annual Report within the meaning of Regulation G. The Company has consistently provided these financial measurements in previous annual reports and the Company’s management believes that these measurements are important to investors and other interested persons, and that investors and such other persons benefit from having a consistent basis for comparison between years and for the comparison with other companies within the industry. These measures may not, however, be comparable to similarly titled measures used by companies outside of the insurance industry. Investors are cautioned not to place undue reliance on these non-GAAP measures in assessing the Company’s overall financial performance.

The Company uses ‘‘operating income’’ or ‘‘operating loss’’ as measures to evaluate the underlying fundamentals of its operations and believes they are a useful measure of its corporate performance. ‘‘Operating income’’ or ‘‘operating loss’’ differs from ‘‘net income available to common shareholders’’ and ‘‘net loss attributed to common shareholders’’, which the Company believes are the most directly comparable GAAP measures, only by the exclusion of net realized gains and losses on investments and, in 2002, by the cumulative effect of a change in accounting principle — goodwill. The Company’s management believes that ‘‘operating income’’ or ‘‘operating loss’’ are useful to investors because they more accurately measure and predict the Company’s results of operations by removing the variability arising from fluctuations in the Company’s investment portfolio and by removing non-recurring matters such as changes in accounting principles — goodwill, which are not considered by management to be a relevant indicator of business operations. The Company also uses operating income or operating loss to calculate operating (loss) income per common share and operating return on average common equity. The following is a reconciliation of 1) net (loss) income available to common shareholders to operating (loss) income available to common shareholders; 2) net (loss) income available to common shareholders per common share to operating (loss) income available to common shareholders per common share; and 3) return on average common equity to operating return on average common equity:

| (In thousands of U.S. dollars) | Year Ended | |||||||||||||||||||||

| 2005 | 2004 | 2003 | 2002 | 2001 | ||||||||||||||||||

| Net (loss) income available to common shareholders | $ | (281,413 | ) | $ | 133,108 | $ | 605,992 | $ | 342,879 | $ | 184,956 | |||||||||||

| Adjustment for net realized losses (gains) on investments | 6,962 | (23,442 | ) | (80,504 | ) | (10,177 | ) | (18,096 | ) | |||||||||||||

| Adjustment for cumulative effect of a change in accounting principle – FAS 142 – Goodwill | — | — | — | 9,187 | — | |||||||||||||||||

| Operating (loss) income | $ | (274,451 | ) | $ | 109,666 | $ | 525,488 | $ | 341,889 | $ | 166,860 | |||||||||||

| Net (loss) income available to common shareholders per common share | (3.99 | ) | $ | 1.85 | $ | 8.53 | $ | 4.88 | $ | 2.96 | ||||||||||||

| Adjustment for net realized losses (gains) on investments | 0.10 | (0.32 | ) | (1.13 | ) | (0.14 | ) | (0.29 | ) | |||||||||||||

| Adjustment for cumulative effect of a change in accounting principle – FAS 142 – Goodwill | 0.13 | |||||||||||||||||||||

| Operating (loss) income per common share – diluted | $ | (3.89 | ) | $ | 1.53 | $ | 7.40 | $ | 4.87 | $ | 2.67 | |||||||||||

| Return on average common equity | (13.6 | %) | 6.2 | % | 33.8 | % | 27.0 | % | 22.1 | % | ||||||||||||

| Adjustment for net realized losses (gains) on investments | 0.3 | % | (1.1 | %) | (4.5 | %) | (0.8 | %) | (2.2 | %) | ||||||||||||

| Adjustment for cumulative effect of a change in accounting principle – SFAS 142 – Goodwill | 0.7 | % | ||||||||||||||||||||

| Operating return on average common equity | (13.3 | %) | 5.1 | % | 29.3 | % | 26.9 | % | 19.9 | % | ||||||||||||

24

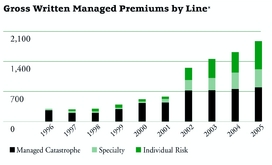

The Company has also included in this Annual Report ‘‘managed catastrophe premium’’ and ‘‘gross written managed premium’’. ‘‘Managed catastrophe premium’’ is defined as gross catastrophe premium written by Renaissance Reinsurance and its related joint ventures. ‘‘Gross written managed premium’’ differs from gross written premium, which the Company believes is the most directly comparable GAAP measure, due to the inclusion of premiums written on behalf of our joint ventures Top Layer Re, which is accounted for under the equity method of accounting, and OPCat, which was accounted for under the equity method of accounting prior to 2002. ‘‘Managed catastrophe premium’’ differs from total catastrophe premium, which the Company believes is the most directly comparable GAAP measure, due to the inclusion of catastrophe premium written on behalf of our joint venture Top Layer Re, which is accounted for under the equity method of accounting, and OPCat, which was accounted for under the equity method of accounting prior to 2002. The following is a reconciliation of 1) total catastrophe premium to managed catastrophe premium; and 2) gross written premium to gross written managed premium:

| Year Ended | ||||||||||||||||||||||

| 2005 | 2004 | 2003 | 2002 | 2001 | ||||||||||||||||||

| Total catastrophe premium | $ | 731,979 | $ | 683,179 | $ | 643,665 | $ | 643,450 | $ | 373,896 | ||||||||||||

| Catastrophe premium written by OPCat | — | — | — | — | 29,129 | |||||||||||||||||

| Catastrophe premium written by Top Layer Re | 59,907 | 70,242 | 76,735 | 73,099 | 38,761 | |||||||||||||||||

| Managed catastrophe premium | $ | 791,886 | $ | 753,421 | $ | 720,400 | $ | 716,549 | $ | 441,786 | ||||||||||||

| Gross written premium | $ | 1,809,128 | $ | 1,544,157 | $ | 1,382,209 | $ | 1,173,049 | $ | 501,321 | ||||||||||||

| Premium written by OPCat | — | — | — | — | 29,129 | |||||||||||||||||

| Premium written by Top Layer Re | 59,907 | 70,242 | 76,735 | 73,099 | 38,761 | |||||||||||||||||

| Gross written managed premium | $ | 1,869,035 | $ | 1,614,399 | $ | 1,458,944 | $ | 1,246,148 | $ | 569,211 | ||||||||||||

The Company has also included in this Annual Report ‘‘tangible book value per share plus accumulated dividends’’. This is defined as book value per share excluding intangible assets, such as goodwill, plus accumulated dividends. ‘‘Tangible book value per share plus accumulated dividends’’ differs from book value per share, which the Company believes is the most directly comparable GAAP measure, due to the exclusion of goodwill and the inclusion of accumulated dividends. The following is a reconciliation of book value per share to tangible book value per share plus accumulated dividends:

| Year Ended | ||||||||||||||||||||||

| 2005 | 2004 | 2003 | 2002 | 2001 | ||||||||||||||||||

| Book value per share | $24.52 | $30.19 | $29.61 | $21.37 | $16.14 | |||||||||||||||||

| Adjustment for goodwill | — | — | — | — | (0.14) | |||||||||||||||||

| Adjustment for accumulated dividends | 5.28 | 4.48 | 3.72 | 3.12 | 2.55 | |||||||||||||||||

| Tangible book value per share plus accumulated dividends | $29.80 | $34.67 | $33.33 | $24.49 | $18.55 | |||||||||||||||||

25

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR

15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For The Fiscal

Year Ended December 31, 2005

Commission File No.

34-0-26512

RENAISSANCERE HOLDINGS LTD.

(Exact Name Of Registrant As Specified In Its Charter)

| Bermuda

(State or Other Jurisdiction of Incorporation or Organization) |

98-014-1974

(I.R.S.Employer Identification Number) |

|||||

Renaissance House, 8-20 East Broadway,

Pembroke HM 19 Bermuda

(Address of Principal Executive

Offices)

(441) 295-4513

(Registrant's

telephone number)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |||||

| Common Shares, Par Value $1.00 per share | New York Stock Exchange, Inc. | |||||

| Series A 8.10% Preference Shares, Par Value $1.00 per share | New York Stock Exchange, Inc. | |||||

| Series B 7.30% Preference Shares, Par Value $1.00 per share | New York Stock Exchange, Inc. | |||||

| Series C 6.08% Preference Shares, Par Value $1.00 per share | New York Stock Exchange, Inc. | |||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if

the registrant is a well-known seasoned issuer (as defined in Rule 405

of the Act). Yes ![]() No

No ![]()

Indicate

by check mark if the registrant is not required to file reports

pursuant to Section 13 or Section 15(d) of the Act. Yes ![]() No

No ![]()

Indicate by check mark whether

the registrant (1) has filed all reports required to be filed by

Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was

required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. Yes ![]() No

No

![]()

Indicate by check mark if disclosure of

delinquent filers pursuant to Item 405 of Regulation S-K is not

contained herein, and will not be contained, to the best of

registrant's knowledge, in definitive proxy or information

statements incorporated by reference in Part III of this Form 10-K or

any amendment to this Form 10-K. ![]()

Indicate by

check mark whether the registrant is a large accelerated filer, an

accelerated filer, or a non-accelerated filer, as defined in Rule 12b-2

of the Act. Large accelerated filer ![]() , Accelerated filer

, Accelerated filer ![]() ,

Non-accelerated filer

,

Non-accelerated filer ![]()

Indicate by check mark

whether the registrant is a shell company (as defined in Rule 12b-2 of

the Act).

Yes ![]() No

No ![]()

The aggregate market value of Common Shares held by nonaffiliates of the registrant at June 30, 2005 was $3,179,508,637 based on the closing sale price of the Common Shares on the New York Stock Exchange on that date.

The number of Common Shares outstanding at February 17, 2006 was 71,546,810.

The information required by Part III of this report, to the extent not set forth herein, is incorporated by reference to the registrant’s Definitive Proxy Statement to be filed in respect of our 2006 Annual General Meeting of Shareholders.

RENAISSANCERE

HOLDINGS LTD.

TABLE OF CONTENTS

| Page | ||||||||||

| PART I. | 1 | |||||||||

| ITEM 1. | BUSINESS | 3 | ||||||||

| ITEM 1A. | RISK FACTORS | 36 | ||||||||

| ITEM 1B. | UNRESOLVED STAFF COMMENTS | 49 | ||||||||

| ITEM 2. | PROPERTIES | 57 | ||||||||

| ITEM 3. | LEGAL PROCEEDINGS | 57 | ||||||||

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS | 58 | ||||||||

| PART II. | 59 | |||||||||

| ITEM 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER REPURCHASES OF EQUITY SECURITIES. | 59 | ||||||||

| ITEM 6. | SELECTED CONSOLIDATED FINANCIAL DATA | 60 | ||||||||

| ITEM 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 63 | ||||||||

| ITEM 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 98 | ||||||||

| ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 99 | ||||||||

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 99 | ||||||||

| ITEM 9A. | CONTROLS AND PROCEDURES | 100 | ||||||||

| ITEM 9B. | OTHER INFORMATION | 100 | ||||||||

| PART III. | 101 | |||||||||

| ITEM 10. | DIRECTORS AND EXECUTIVE OFFICERS OF RENAISSANCERE | 101 | ||||||||

| ITEM 11. | EXECUTIVE COMPENSATION | 101 | ||||||||

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED SHAREHOLDER MATTERS | 101 | ||||||||

| ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 101 | ||||||||

| ITEM 14. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 101 | ||||||||

| PART IV. | 102 | |||||||||

| ITEM 15. | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 102 | ||||||||

| Signatures | 107 | |||||||||

PART I

Unless the context otherwise requires, references in this Annual Report to ‘‘RenaissanceRe’’ or the ‘‘Company’’ mean RenaissanceRe Holdings Ltd. and its subsidiaries, which principally include Renaissance Reinsurance Ltd. (‘‘Renaissance Reinsurance’’), Renaissance Reinsurance of Europe (‘‘Renaissance Europe’’), Glencoe Group Holdings Ltd. (‘‘Glencoe Group’’), Glencoe Insurance Ltd. (‘‘Glencoe’’), Glencoe U.S. Holdings Inc. (‘‘Glencoe U.S.’’), Stonington Insurance Company (‘‘Stonington’’), Lantana Insurance Ltd. (‘‘Lantana’’), Glencoe Group Services Inc. ("Glencoe Group Services’’), Renaissance Underwriting Managers, Ltd.(‘‘RUM’’), RenaissanceRe Ventures Ltd. (‘‘Ventures’’), RenaissanceRe Capital Trust (‘‘Capital Trust’’), Renaissance Investment Management Company Ltd. (‘‘RIMCO’’), Renaissance Investment Holdings Ltd. (‘‘RIHL’’) and RenaissanceRe Services Ltd. We also underwrite reinsurance on behalf of joint ventures, principally including Top Layer Reinsurance Ltd. (‘‘Top Layer Re’’) and DaVinci Reinsurance Ltd. (‘‘DaVinci’’). DaVinci’s financial results are consolidated in our financial statements. Unless the context otherwise requires, references to RenaissanceRe do not include any of the joint ventures for which we provide underwriting services. Certain terms used below are defined in the ‘‘Glossary of Selected Insurance Terms’’ appearing on page 50 of this Form 10-K.

NOTE ON FORWARD-LOOKING STATEMENTS

This Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the ‘‘Exchange Act’’). Forward-looking statements are necessarily based on estimates and assumptions that are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which, with respect to future business decisions, are subject to change. These uncertainties and contingencies can affect actual results and could cause actual results to differ materially from those expressed in any forward-looking statements made by, or on behalf of, us.

In particular, statements using words such as ‘‘may,’’ ‘‘should,’’ ‘‘estimate,’’ ‘‘expect,’’ ‘‘anticipate,’’ ‘‘intends,’’ ‘‘believe,’’ ‘‘predict,’’ ‘‘potential’’ or words of similar import generally involve forward-looking statements. For example, we have included certain forward-looking statements in ‘‘Management's Discussion and Analysis of Financial Condition and Results of Operations’’ with regard to trends in results, prices, volumes, operations, investment results, margins, combined ratios, reserves, overall market trends, risk management and exchange rates. This Form 10-K also contains forward-looking statements with respect to our business and industry, such as those relating to our strategy and management objectives, trends in market conditions, prices, market standing and product volumes, investment results and pricing conditions in the reinsurance and insurance industries.

In light of the risks and uncertainties inherent in all future projections, the inclusion of forward-looking statements in this report should not be considered as a representation by us or any other person that our objectives or plans will be achieved. Numerous factors could cause our actual results to differ materially from those addressed by the forward-looking statements, including the following:

| • | we are exposed to significant losses from catastrophic events and other exposures that we cover that may cause significant volatility in our financial results; |

| • | the frequency and severity of catastrophic events could exceed our estimates and cause losses greater than we expect; |

| • | risks associated with implementing our business strategies and initiatives, including risks relating to effecting our leadership transition; |

| • | risks associated with executing our strategy in our newer specialty reinsurance and Individual Risk businesses, including the development of our infrastructure to support these lines; |

| • | risks relating to our strategy of relying on program managers, third-party administrators, and other vendors to support our Individual Risk operations; |

| • | other risks of doing business with program managers, including the risk we might be bound to policyholder obligations beyond our underwriting intent, and the risk that our program managers or agents may elect not to continue or renew their programs with us; |

1

| • | risks that the current governmental investigations or related proceedings involving the Company might impact us adversely, including as regards our senior executive team; |

| • | the risk of the lowering or loss of any of the ratings of RenaissanceRe or of one or more of our subsidiaries or changes in the policies or practices of the rating agencies; |

| • | risks that we may require additional capital in the future, in particular after a catastrophic event, which may not be available or may be available only on unfavorable terms; |

| • | the inherent uncertainties in our reserving process, including those related to the 2005 catastrophes, which uncertainties we believe are increasing as we diversify into new product classes; |

| • | the risk that ongoing or future industry regulatory developments will disrupt our business, or that of our business partners, or mandate changes in industry practices in ways that increase our costs, decrease our revenues or require us to alter aspects of the way we do business; |

| • | risks relating to the availability and collectibility of our reinsurance with respect to both our Reinsurance and Individual Risk operations; |

| • | failures of our reinsurers, brokers or program managers to honor their obligations, including their obligations to make third-party payments for which we might be liable; |

| • | emerging claims and coverage issues, which could expand our obligations beyond the amount we intend to underwrite; |

| • | we may be affected by increased competition, including from new entrants being formed following hurricane Katrina, or in future periods by a decrease in the level of demand for our reinsurance or insurance products; |

| • | acts of terrorism, war or political unrest; |

| • | possible challenges in maintaining our fee-based operations, including risks associated with retaining our existing partners and attracting potential new partners; |

| • | a contention by the U.S. Internal Revenue Service that our Bermuda subsidiaries, including Renaissance Reinsurance, Glencoe and RIHL, are subject to U.S. taxation; |

| • | loss of services of any one of our key executive officers, or difficulties associated with the transition of new members of our senior management team; |

| • | changes in economic conditions, including interest rate, currency, equity and credit conditions which could affect our investment portfolio; |

| • | sanctions against us, as a Bermuda-based company, by multinational organizations; |

| • | extraordinary events affecting our clients or brokers, such as bankruptcies and liquidations, and the risk that we may not retain or replace our large clients; |

| • | changes in the distribution or placement of risks due to increased consolidation of insurance and reinsurance brokers, or program managers, or from potential changes in their business practices which may be required by future regulatory changes; |

| • | changes in insurance regulations in the U.S. or other jurisdictions in which we operate, including potential challenges to Renaissance Reinsurance's claim of exemption from insurance regulation under current laws, the risk of increased global regulation of the insurance and reinsurance industry, and the risk that TRIA will not be renewed after 2007; |

| • | the passage of federal or state legislation subjecting Renaissance Reinsurance or our other Bermuda subsidiaries to supervision, regulation or taxation in the U.S. or other jurisdictions in which we operate; and |

| • | operational risks, including system or human failures. |

2

The factors listed above should not be construed as exhaustive. Certain of these factors are described in more detail in ‘‘Risk Factors’’ below. We undertake no obligation to release publicly the results of any future revisions we may make to forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

ITEM 1. BUSINESS

GENERAL

RenaissanceRe was established in Bermuda in 1993 to write property catastrophe reinsurance. Through our operating subsidiaries, we seek to obtain a portfolio of reinsurance, insurance and financial risks in each of our businesses that is significantly better than the market average and produces an attractive return on equity. Our strategy focuses on superior risk selection, active capital management, superior utilization of risk management and information systems, the development and enhancement of a high performance and ethical culture and our commitment to our clients and joint venture partners. We provide value to our clients in the form of financial security, innovative products, and responsive service. We are known as a leader in paying valid reinsurance claims promptly. We measure our financial success through long-term growth in tangible book value per common share plus accumulated dividends and believe we have delivered superior performance in this regard in the past.

Our core products include property catastrophe reinsurance, which we write through our principal operating subsidiary Renaissance Reinsurance and joint ventures, principally DaVinci and Top Layer Re; specialty reinsurance risks through Renaissance Reinsurance and DaVinci; and primary insurance and quota share reinsurance, which we write through the operating subsidiaries of the Glencoe Group. We believe that we are one of the world’s largest writers of property catastrophe reinsurance based on gross managed premiums written. We also believe we have a strong position in certain specialty reinsurance lines of business and are building a unique franchise in the U.S. program business. Our reinsurance and insurance products are principally distributed through intermediaries, with whom we seek to cultivate strong relationships.

We conduct our business through two reportable segments, Reinsurance and Individual Risk. For the year ended December 31, 2005, our Reinsurance and Individual Risk segments accounted for approximately 64.0% and 36.0%, respectively, of our total consolidated gross premiums written. The share attributable to Individual Risk premiums has increased significantly over the last three years. Our segments are more fully described in ‘‘Business Segments’’ below.

Risk Management and Underwriting

A principal focus of RenaissanceRe is to develop and effectively utilize sophisticated computer models and other analytical tools to assess the risks that we underwrite and optimize our portfolio of reinsurance and insurance contracts. These efforts are managed across our organization by a team of professionals led by our chief underwriting officer.

With respect to our Reinsurance operations, since 1993 we have developed a proprietary, computer-based pricing and exposure management system, Renaissance Exposure Management System (REMS©). As described in more detail below, we believe that REMS© is a more robust underwriting and risk management system than is currently commercially available elsewhere in the reinsurance industry and offers us a significant advantage amongst our competitors. REMS© was developed to analyze catastrophe risks, and is being developed to analyze other classes of risk.

In addition to using REMS©, within our Individual Risk operations we have developed a proprietary information management and analytical database (Program Analysis Central Repository or ‘‘PACeR’’), within which data related to substantially all our U.S. program business is maintained. With the use and development of PACeR, we are seeking to develop statistical and analytical techniques to evaluate our U.S. program lines of business. We provide our clients with access to PACeR and believe it helps them understand their business and make better underwriting decisions, thus creating value for them and for us. Our objective is to have PACeR create an advantage for our Individual Risk operations by assisting us in building and maintaining a well-priced portfolio of specialty insurance risks.

3

New Business

In addition to the potential growth of our existing reinsurance and insurance businesses, from time to time we consider opportunistic diversification into new ventures, either through organic growth, the formation of new joint ventures, or the acquisition of other companies or books of business of other companies. This potential diversification includes opportunities to write targeted classes of non-catastrophe business, both directly for our own account and through possible new joint venture opportunities.

In evaluating such new ventures, we seek an attractive return on equity, the ability to develop or capitalize on a competitive advantage, and opportunities that will not detract from our core Reinsurance and Individual Risk operations. Accordingly, we regularly review strategic opportunities and periodically engage in discussions regarding possible transactions, although there can be no assurance that we will complete any such transactions or that any such transaction would contribute materially to our results of operations or financial condition.

Legal Matters

In the fourth quarter of 2004, we commenced a review of the Company’s business practices in light of the industry-wide investigations by the Office of the Attorney General for the State of New York (the "NYAG") and other government authorities into a wide range of practices in the insurance and reinsurance industry. In February 2005, we announced that we had determined to restate the Company’s financial statements for the fiscal years ended December 31, 2003, 2002 and 2001. Thereafter we received subpoenas from, and are the subject of ongoing investigations by, the Securities and Exchange Commission (‘‘SEC’’), the United States Attorney's Office for the Southern District of New York and the NYAG, as well as civil suits arising out of the events and circumstances which are the subjects of those subpoenas and investigations. In connection with these investigations, in July 2005, James N. Stanard, the Company’s then Chairman and Chief Executive Officer (‘‘CEO’’), received a Wells Notice from the staff of the SEC in connection with the SEC’s investigation. The Company understands that Michael W. Cash, a former officer of the Company, also received a Wells Notice at about that time. In addition, in September 2005, the Company received a Wells Notice in connection with the SEC’s investigation. The Wells Notices indicate that the staff intends to recommend that the SEC bring a civil enforcement action against the recipients alleging violations of federal securities laws and that the staff may seek permanent injunctive relief, civil penalties or disgorgement. We are unable to predict the ultimate outcome of these investigations, which could result in injunctive relief, penalties, require remediation, or otherwise impact the Company and/or our senior management team in a manner which may be adverse to us, perhaps materially so. We intend to continue to cooperate with these investigations. See ‘‘Legal Proceedings.’’

On November 1, 2005, we announced the resignation of Mr. Stanard as our Chairman and CEO and that Neill A. Currie had been named by the Board of Directors as our new CEO and had also been appointed to the Board of Directors, and that W. James MacGinnitie had been appointed non-executive Chairman of the Board of Directors. Following this announcement, Standard & Poor's Ratings Services, Moody's Investors Service Inc., Fitch Ratings Ltd., and A.M. Best Company, Inc. downgraded certain of the ratings of our principal operating subsidiaries and joint ventures and the senior debt ratings of the Company. Our ratings generally remain on watch with these agencies. See ‘‘Management’s Discussion and Analysis of Financial Condition and Results of Operations – Capital Resources – Credit Ratings’’ and ‘‘Legal Proceedings.’’

4

CORPORATE STRATEGY

We seek to generate long-term growth in tangible book value per common share plus accumulated dividends for our shareholders by pursuing the following strategic objectives:

| • | Superior Risk Selection. We seek to underwrite our reinsurance, insurance and financial risks through the use of sophisticated risk selection techniques, including computer models. We pursue a disciplined approach to underwriting and only select those risks that we believe will produce an attractive return on equity, subject to prudent risk constraints. |

| • | Marketing. We believe our modeling and technical expertise, and the risk management advice that we provide to our clients, has enabled us to become a provider of first choice in many lines of business to our customers worldwide. We market our Reinsurance products worldwide exclusively through reinsurance brokers. We seek to offer stable, predictable and consistent risk-based pricing. We seek to achieve a prompt turnaround on our claims. |

| • | Active Capital Management. We aim to write as much attractively priced business as is available and then manage our capital accordingly. We typically seek to raise capital when we expect an increase in attractively priced business and return capital to our shareholders or joint venture investors when the amount of attractively priced business declines. |

| • | Joint Ventures. Building upon our relationships and expertise in risk selection, marketing and capital management, we have successfully established new joint venture and investment opportunities, which include new partners and diversifying classes of business. We intend to pursue additional joint venture opportunities. |

We believe we are positioned to fulfill these objectives by virtue of the experience and skill of our management team, our significant financial strength, and our strong relationships with brokers and clients. In addition, we believe our superior service, our proprietary modeling technology, and our extensive business relationships which have enabled us to become a leader in the property catastrophe reinsurance market will be instrumental in allowing us to achieve our strategic objectives.

BUSINESS SEGMENTS

We conduct our business through two reportable segments, Reinsurance and Individual Risk. Financial data relating to our two segments is included in Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations and in our Consolidated Financial Statements and Notes presented under Item 8.

Reinsurance Segment

Our Reinsurance operations are comprised of three components: 1) property catastrophe reinsurance, primarily written through Renaissance Reinsurance and DaVinci; 2) specialty reinsurance, primarily written through Renaissance Reinsurance and DaVinci; and 3) certain other activities of Ventures as described herein. Our Reinsurance operations are managed by the President of Renaissance Reinsurance, who leads a team of underwriters, risk modelers and other industry professionals, who have access to our proprietary risk management, underwriting and modeling resources and tools. We believe the expertise of our underwriting and modeling team and our proprietary analytic tools, together with superior customer service, provide us with a significant competitive advantage.