SLIDES FOR PRESENTATION

Published on September 18, 2007

RenaissanceRe Holdings Ltd.

Investor Presentation

September 2007

Table of Contents

Consistent Strategy

Identifying Opportunities

Leveraging Our Franchise

Recent Developments

Well-Positioned for the Future

Our focus and strategy remain the same

We focus on four key business areas

Property Cat Reinsurance

Specialty Reinsurance

Individual Risk

Joint Ventures and Strategic Investments

Four core strategies are key to our success

Superior risk selection underwriting discipline, proprietary tools, risk

management culture

Superior marketing to get the business that we select

Superior capital management to match capital with risk

Superior joint ventures- to maximize capital efficiency for clients, capital providers

and RNR shareholders

3

Key Competitive Advantages

Discipline - Disciplined underwriter with proven track record in hard and soft

markets; history of identifying market inefficiencies

Talent & Culture - Experienced management team; risk management culture;

shared strategic vision

Use Of Technology Proprietary models to analyze and aggregate risk; large

databases to support decision making; recognize

limits of modeling

Relationships - Excellent customer and broker relationships; recognized market

leader; focus on adding value

Capital - Strong capitalization; strong loss reserves; multiple channels by which to

access capital; disciplined capital management

4

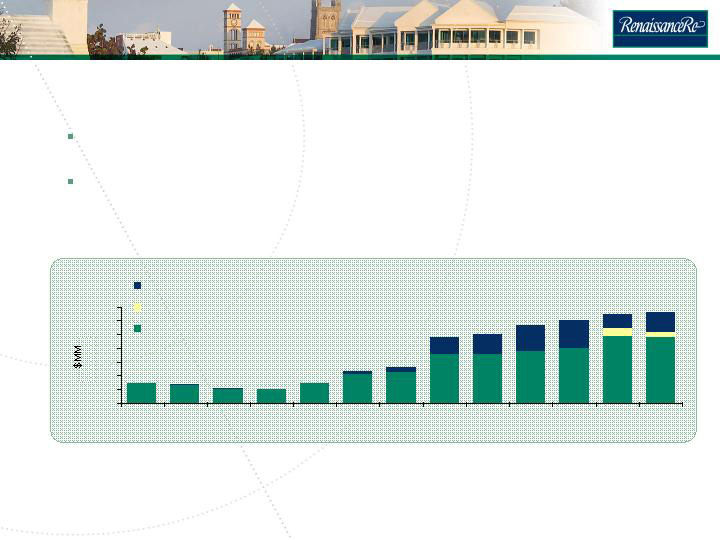

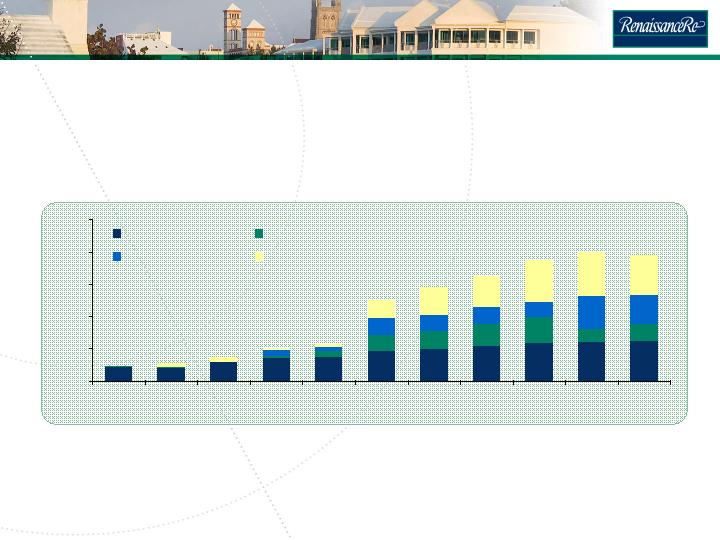

Discipline requires knowing when to grow and when

to shrink

Market conditions dictate writings we decrease when conditions soften

(e.g. late 90s), and grow when pricing improves (e.g. 2002)

Specialty declined in 2006 as we stayed disciplined in a more competitive market,

but there were attractive prospects to grow in our core Cat business

0

200

400

600

800

1000

1200

1400

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Proj.

Specialty

Managed Cat ceded to fully-collateralized J.V.'s

Managed Cat

Projected as of Q2

Information concerning the reconciliation of Non-GAAP measures can be found at the end of this presentation.

*2007 projected Managed Catastrophe and Specialty Premiums are based on August 2007 premium estimates of managed catastrophe

premiums down 5%, Individual Risk premiums down 10% and specialty reinsurance premiums

written up 35%.

Managed Catastrophe and Specialty Premiums

5

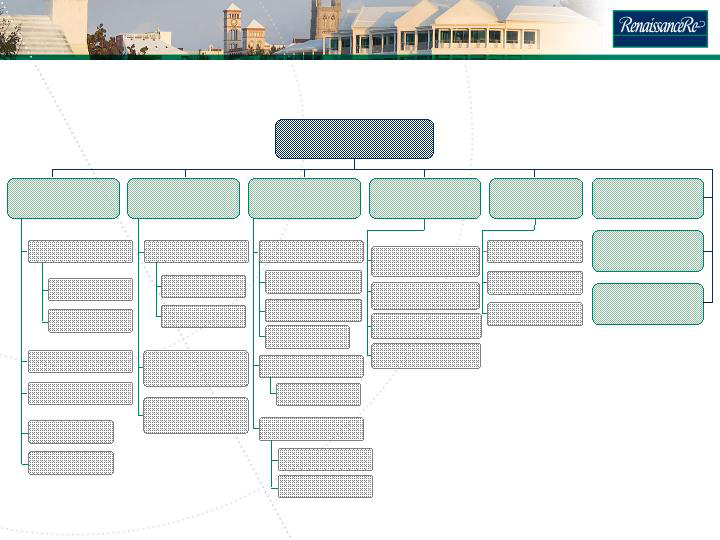

Our team is strong and key to our success

US Underwriting SVP

International

Underwriting SVP

Kevin J. O'Donnell

President

Renaissance Reinsurance

Corporate Risk

VP

Senior Development

Analyst VP

Risk Modeling SVP

RenRe

Investment Managers

President

Weather Predict

President

William I. Riker (1)

President

Chief Underwriting Officer

President GUSH

CFO GUSH

William J. Ashley

CEO

Glencoe Group

RenaissanceRe Ventures

SVP

John D. Nichols

EVP, President

RenaissanceRe Ventures

Chief Accting Officer

Controller SVP

Treasurer

(Open)

Internal Audit

VP

Fred R. Donner

Chief Financial Officer

EVP

Stephen H. Weinstein

General Counsel, SVP

Chief Compliance Officer

Peter C. Durhager

Chief Administrative

Officer SVP

Todd R. Fonner

CRO and CIO

SVP

Neill A. Currie

Chief Executive Officer

US Underwriting

VP

US Underwriting

VP

Specialty

Underwriting SVP

General Counsel

GUSH

GUSH Modeling VP

COO GUSH

Program Operations

SVP

Specialty

Underwriting VP

Specialty

Underwriting VP

RenaissanceRe Ventures

SVP

Business Development

SVP

Business Development

SVP

GUSH Claims VP

(1) Mr. Riker will remain with the Company until the end of 2007, and thereafter remain an employee serving in an advisory capacity until August 2008. Neill A. Currie, Chief Executive Officer of RenaissanceRe, will also assume the role of President.

RenaissanceRe Ventures

VP

RenaissanceRe Ventures

VP

6

We are differentiated in the resources we dedicate

to risk modeling

Risk Modeling

Resources

Reinsurance (11)

6 Modelers

1 Actuary

2 Masters

Individual Risk (6)

Risk Systems (5)

1 Masters

4 Programmers

WPC Consulting (14)

12 Ph.Ds

RIM (5)

3 Ph.Ds

Corporate Risk (3)

3 MBAs

Quant. Group (4)

1 Ph.D

1 Masters

3 Masters

7

Risk management is more than modeling

management expertise and corporate culture are critical

Avoid

Surprises

Proactive

Response

to Market

Opportunities

Superior Risk Management

Highly talented

individuals

Underwriters

understand models

Clear accountability

Tight control

of authority

Peer review

Ownership mentality

REMS©

Computer

System

Clean database

User friendly

system

Multiple vendor

models

Many unique

custom features

Management

Procedures

and Culture

8

To manage capital we cultivate diversified

and flexible sources

Multiple channels of access for capital is

a competitive advantage

Retrocessional reinsurance capacity

can be used to manage capital needs

when available at economic terms

Bank debt can be used to manage

capital quickly; short timeframe to

access with no prepayment penalties

Joint ventures with private capital

enhance our ability to manage capital

flexibly; capital comes in and out at

book value

Soft capital can be targeted short-term

at the most dislocated part of the market

to create capacity for incremental

business

RNR

Long-term

JV Capital

e.g. DaVinci

Public

Equity

Reinsurance

Public

Debt

Short-term

Soft Capital

e.g.

Starbound I&II

Private/

Bank Debt

9

Our goal remains long-term growth in tangible book

value per share plus accumulated dividends

Tangible book value per share plus accumulated dividends has grown at an

annualized rate of 17.5% from 1997 through 2006 driven by a track record of

strong Operating ROE

While the 2004 and 2005 results were disappointing, 2005s result is consistent

with our models that indicate we should expect to lose money every ten to fifteen

years

Operating ROE*

Tangible Book Value Per Share plus

Accumulated Dividends*

* Information concerning the reconciliation of Non-GAAP measures can be found at the end of this presentation.

10

We are also well-positioned to address the new sources of capital

that are entering our business

Hedge funds, investment banks and securitization have increasingly become

sources of risk-bearing capacity for property catastrophe risks we

believe

further growth is inevitable

These participants will change the way our business is transacted

Real-time trading of the underlying risk should emerge

Indices and other standardized formats for assuming risk will continue to gain

market share

Capital will flow in and out of our business more quickly as market conditions

change

Our Ventures and RIM business units are important components of a strategy to

keep pace with this change

Our Ventures unit has developed key skills and capabilities as an intermediary

for and transformer of Cat risk

11

Table of Contents

Consistent Strategy

Identifying Opportunities

Leveraging Our Franchise

Recent Developments

Well-Positioned for the Future

While our strategy will remain consistent,

our business focus will evolve

We operate today with the same culture and principles as when

the company was formed

By staying disciplined and focused we have been able to leverage our approach

to build a more diversified business model

We will continue to evaluate new opportunities and hope to add additional

franchises, but are committed to maintaining our culture and our standards

for growing book value per share

We will only add businesses that earn attractive risk-adjusted

returns and will exit businesses that no longer do the same

13

We screen new opportunities with a consistent

framework

We look for new business opportunities that meet our return hurdles and fit our

business model.

Credible Data/

Decision Support

Tools

Market

Opportunity

Cultural Fit

14

Weve used this approach to grow from a Cat company

to four successful business units

0

500

1,000

1,500

2,000

2,500

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Proj.

RenRe Cat

RenRe Specialty

Joint Venture

Individual Risk

Projected as of Q2

* Information concerning the reconciliation of Non-GAAP measures can be found at the end of this presentation.

Gross written managed premium

15

Table of Contents

Consistent Strategy

Identifying Opportunities

Leveraging Our Franchise

Recent Developments

Well-Positioned for the Future

We are leveraging off of our market leading franchise

in Property Cat

Consistent pricing

Quick response

Customized products

Capacity for large lines

Advice on Cat risk management

Superior credit quality and

willingness to pay

Normal open market position

Plus preferred signings on open

market transactions

Plus private market transactions

Option to renew business

written for fully collateralized

vehicles

RNR delivers value

RNR gets preferred status

17

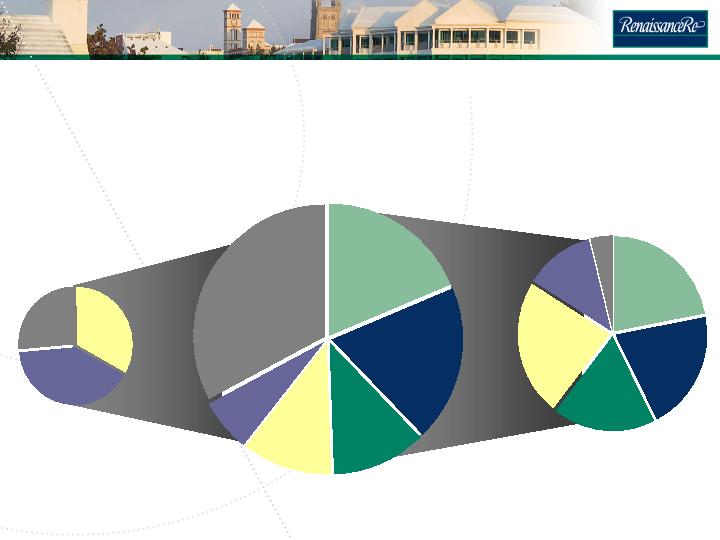

2001 Specialty Premium

$77 million

2006 Specialty Premium

$222 million

2005 Specialty Premium

$427 million

33.1%

40.6%

26.3%

32.7%

18.7%

19%

6.7%

11.1%

11.8%

12%

4%

23%

18%

22%

21%

Since 2001, weve built a more diversified Specialty Re portfolio

while remaining disciplined in 2006s softening market

18

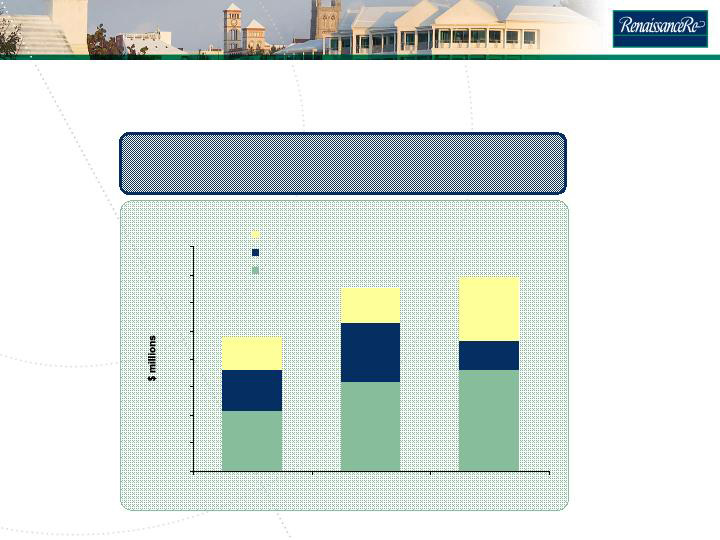

Individual Risk has grown significantly

$0

$100

$200

$300

$400

$500

$600

$700

$800

2004

2005

2006

Commercial Property

Personal Lines Property

Commercial Multi -Lines

Individual Risk Gross Written Premium

by Major Type of Business

19

Individual Risk is selectively focused with a small group

of partners

Our Individual Risk Unit is focused on high-margin primary insurance and quota

share reinsurance where we evaluate the Individual Risk (i.e. underwriting

policies as distinguished from portfolios)

We partner with other insurance companies and program managers

(intermediaries) who source the risk and provide back office support

We target a small number of partners with the following characteristics:

Leaders in their classes of risk

Large premium volume

Efficient back offices

Focused on data, systems and rigorous risk analytics

We are developing proprietary risk modeling tools to track and evaluate exposures

20

Ventures has developed three areas of competence

Catastrophe Portfolio

Participation CPPs -

Participation in the results

of our Property Cat book

Starbound I & II (Florida)

Timicuan Re (Florida)

Cat Bonds

Other

Platinum (2002) IPO spin-off

of St. Pauls reinsurance

operations

ChannelRe Holdings Ltd.

(2004) Financial guarantee

reinsurer in partnership with

MBIA, Partner Re and Koch

Financial

Tower Hill (2005) -

Recapitalization of Florida

primary insurance companies

Top Layer Re

DaVinci Re

OPCat

Examples

Custom packaging

and selling of risk

Strategic investments to

capitalize upon market

dislocations

Attractive businesses that we

prefer to invest in rather than

operate

Continue to selectively

consider large deals or other

classes of business

Leveraging RenRes

capabilities and reputation

as the leading Property Cat

reinsurer

Very active role in the

management, oversight

and corporate governance

of the entities

Business

3) Customized Reinsurance

2) Strategic Investments

1) Property Cat Joint Ventures

21

The period following the 2004 and 2005 storms highlighted

the importance of Ventures role within RenaissanceRe

In 2006 and 2007 we executed four significant capital raises to bring capacity to

our clients

Our joint venture track record since 1999 demonstrates RenaissanceRes ability to

add value = generate alpha

We expanded on our inventory of relationships with investors and advisors

Our reputation with our clients, the option value of the renewal business and the

fee income will benefit us for years into the future

We remain differentiated in our approach and the resources we dedicate which

leaves us well positioned

22

Table of Contents

Consistent Strategy

Identifying Opportunities

Leveraging Our Franchise

Recent Developments

Well-Positioned for the Future

Recent developments

July U.K. floods- Industry loss estimate

*£1 billion-*£1.5 billion. Our preliminary

loss estimate is not

expected to be material.

Hurricane Dean- Industry loss estimate

*$750 million-*$1.5 billion. Our

preliminary loss estimate is not expected to

be material.

Hurricane Felix- Industry loss estimate minimal at less than

*$200 million. Our

preliminary loss estimate is not expected to be material.

Capital Management- Active10b5-1

plan year to date share repurchases totaled

$88.2 million of which 3rd quarter to date share repurchases totaled $77.1 million.

*Source Risk Management Solutions (RMS)

24

Table of Contents

Consistent Strategy

Identifying Opportunities

Leveraging Our Franchise

Recent Developments

Well-Positioned for the Future

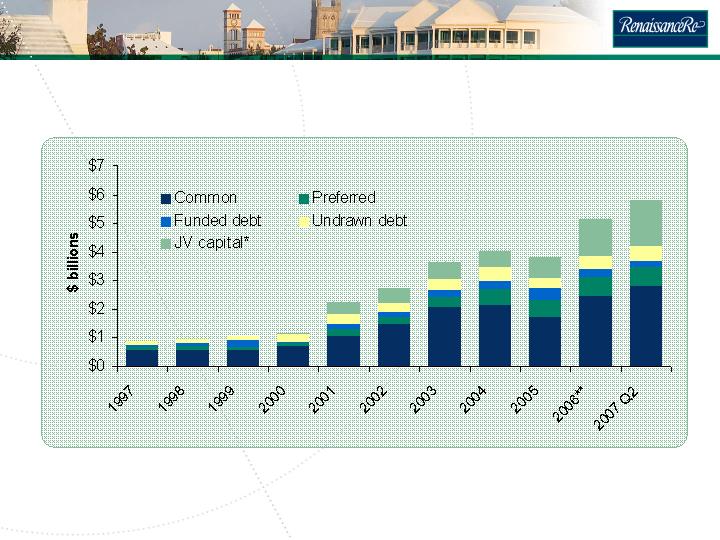

Our balance sheet and capital base are strong

* excluding $3.9 billion of capacity at Top Layer Re

**Reflects the redemption of ~$250 million of preference shares and funded debt, which were redeemed during Q1 2007.

26

RenaissanceRe is well-positioned

Our balance sheet and capital base are strong - our capital position is stronger

than at any point in our history

Our culture and talented team remain a key competitive advantage

We have strengthened our position over the last year as the market leader in

property cat reinsurance; ahead of peers on risk analytics

We are well positioned for the remainder of 2007 but we will remain disciplined

and will not seek growth unless we find attractive opportunities

27

Safe Harbour Statement

Cautionary Statement under "Safe Harbor Provisions of the Private Securities Litigation Reform

Act of 1995:

Statements made in this presentation contain information about the Company's future business

prospects. These statements may be considered "forward-looking." These statements are subject

to

risks and uncertainties that could cause actual results to differ materially from those set forth in

or implied by such forward-looking statements. For further information regarding cautionary

statements and factors affecting future results, please

refer to RenaissanceRe Holdings Ltd.s

filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for

the year ended December 31, 2006 and its Form 10-Qs for the quarters ended March 31, 2007 and

June 30,

2007.

This presentation includes certain non-GAAP financial measures within the meaning of Regulation

G including "operating return on equity", "tangible book value per share plus accumulated

dividends

and gross written managed premium. A definition of such measures and a

reconciliation of these measures to the most comparable GAAP figures in accordance with

Regulation G is available in the Company's 2006, 2005, 2004

and 2003 Annual Reports and the

February 6, 2007, May 1, 2007 and July 31, 2007 Press Releases which are located on the

Company's website

www.renre.com

28

RenaissanceRe Holdings Ltd.

Renaissance House

8 20 East Broadway

Pembroke, HM 19

Bermuda

Tel: (441) 295-4513

www.renre.com