SLIDE PRESENTATION

Published on February 23, 2009

RenaissanceRe Holdings Ltd. Merrill Lynch Insurance Investor Conference February 2009 Exhibit 99.2 |

2 Safe Harbor Statement Cautionary Statement under "Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995: Statements made in this presentation contain information about the Company's future business prospects. These statements may be considered "forward-looking." These statements are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by such forward-looking statements. Forward-looking statements are only as of the date they are made and we do not undertake any obligation to update or revise publicly any

forward- looking statements, whether as a result of new information,

future events or otherwise. For further information regarding cautionary

statements and factors affecting future results, please refer to RenaissanceRe Holdings Ltd.s filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2008. This presentation includes certain non-GAAP financial measures within the meaning of

Regulation G including "tangible book value per common share plus accumulated dividends and managed catastrophe premium. A definition of such measures and a reconciliation of these measures to the most comparable GAAP figures in accordance with Regulation G is available in the Company's February 11, 2009 Earnings Release and Financial Supplement which are located on the Company's website www.renre.com under Investor Information/Current News and Investor Information/Financial Reports respectively. |

Table

of Contents Holdings Overview: A Consistent Strategy Reinsurance: Market Leading Franchise Individual Risk: Building Out Our Platform Ventures: Leveraging and Expanding Our Franchise Hurricane Science: Extending Scientific Leadership Financial Profile: Strong Capital and Liquidity Position Summary: Well-Positioned for the Future |

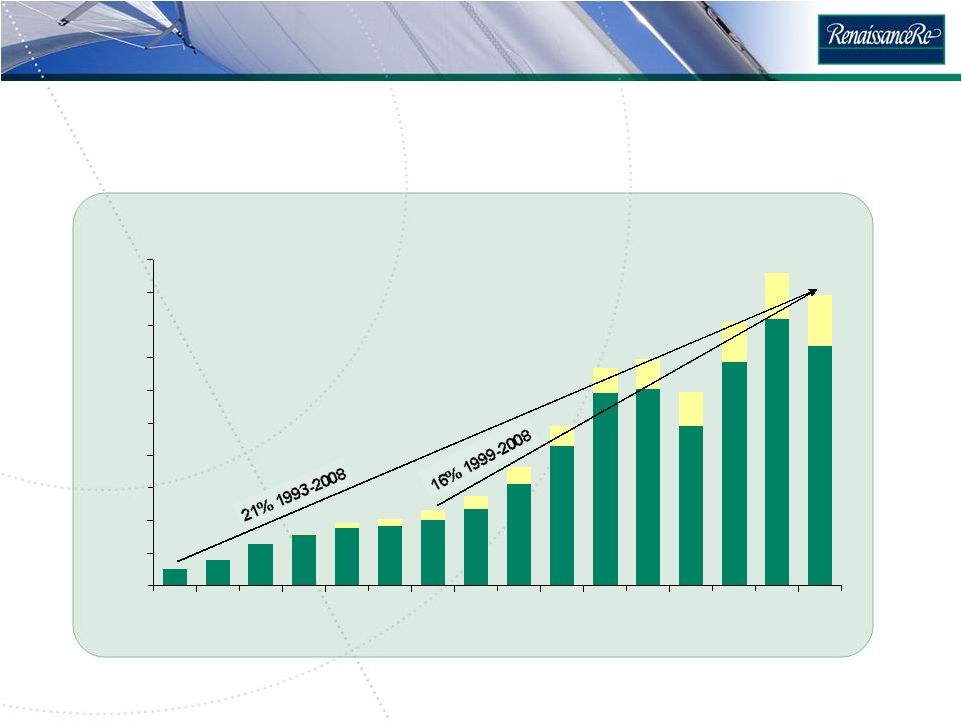

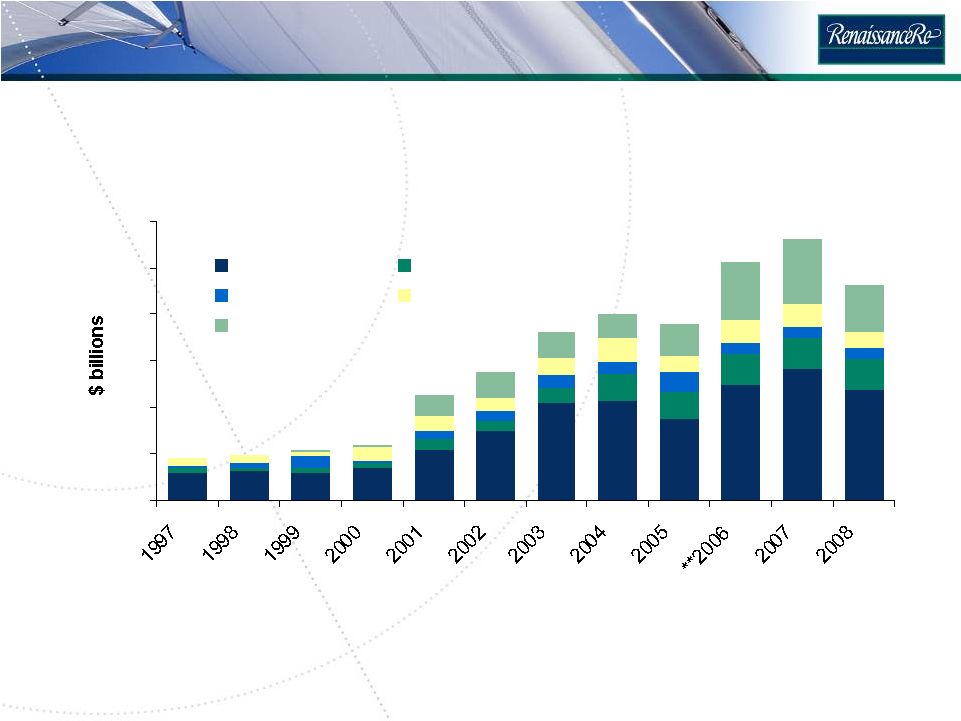

We

have generated superior shareholder value across market cycles 4 Legend: Green =TBVPS; Yellow = accumulated dividends *Information concerning the reconciliation of Non-GAAP measures can be found at the

beginning of this presentation.

$0 $5 $10 $15 $20 $25 $30 $35 $40 $45 $50 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Tangible Book Value Per Common Share plus Accumulated Dividends* |

5 Our focus remains the same We focus on four key business areas

Property Cat Reinsurance Specialty Reinsurance Individual Risk Joint Ventures and Strategic Investments |

6 Our consistent strategy provides us with important competitive advantages Confidence to quote risks in changing environment Long term outperformance Normal open market position - Plus preferred signings on open market transactions - Plus private market transactions Higher market share of attractive business Focus on underwriting Ability to expand and contract capital in innovative ways Creates opportunities for capital providers and capital available to clients Optimize return to investors Consistent exposure based pricing Quick response Customized products Capacity for large lines Advice on cat risk management Superior credit quality and willingness to pay Excellent financial rating Multiple channels of access to capita Innovation Matching capital to risk Joint ventures Underwriting excellence Premiere risk modeling capabilities and technology |

7 Multiple channels of access to capital is a competitive advantage RNR Long-term JV Capital (e.g. DaVinci) Public Equity Reinsurance Public Debt Short-term or Soft Capital (e.g. Starbound I

& II) Private/ Bank Debt |

8 We screen new opportunities with a consistent framework We look for new business opportunities that meet our return hurdles and fit our

business model. Credible Data/ Decision Support Tools Market Opportunity Cultural Fit |

9 Extending our industry leadership: different approaches to different cycles Pedal to the metal in existing business Innovate to create capacity / opportunity, working with Ventures business: - Sidecars - Parametric solutions Maintain discipline around exposure-based pricing Define value proposition for brokers / buyers Strengthen existing business operations Maintain discipline around exposure based pricing - Deal we will do versus offered terms Cautiously pursue new opportunities Return capital to shareholders Hard Market Strategies Soft Market Strategies |

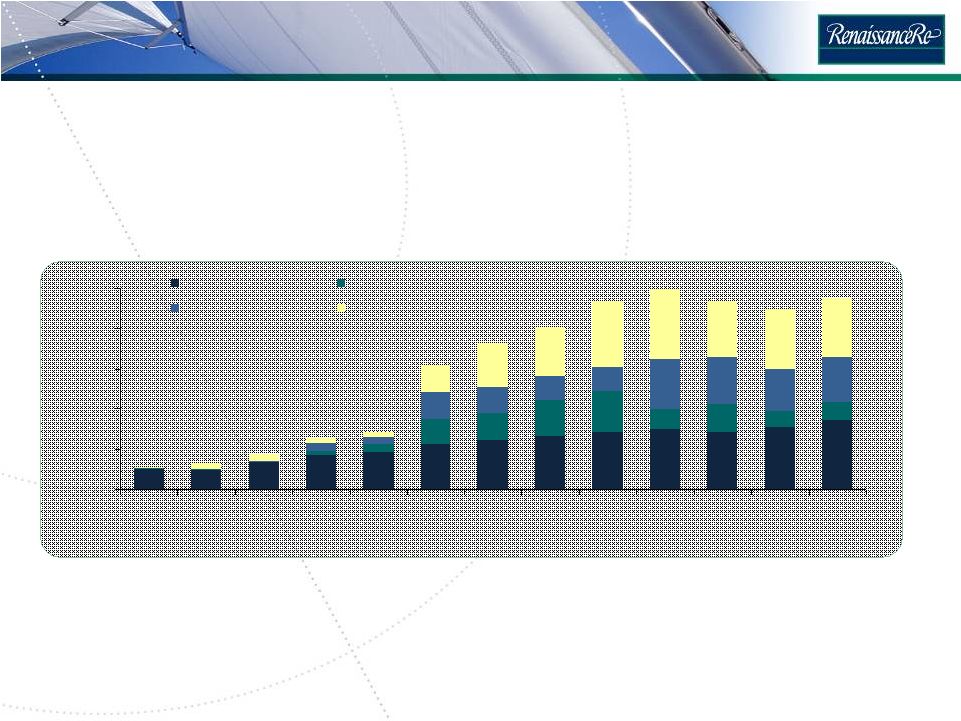

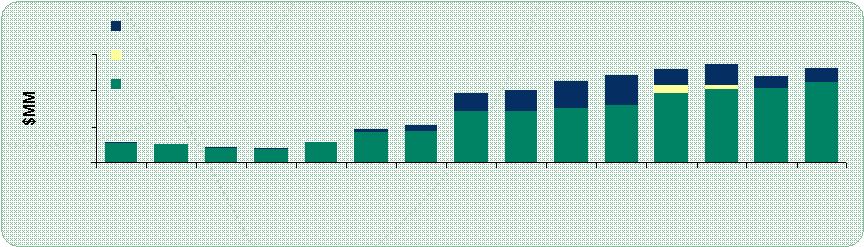

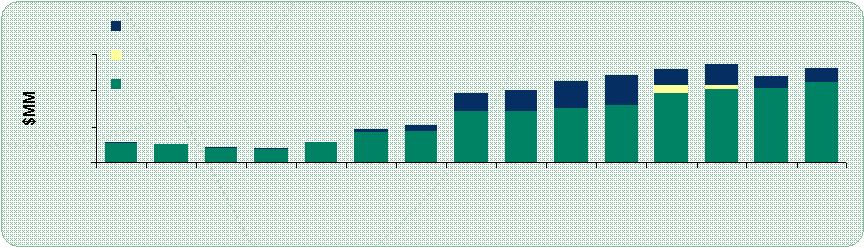

10 Our expansion strategy has been key to our growth 0 400 800 1,200 1,600 2,000 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 (proj. 1) RenRe Cat RenRe Specialty Joint Venture* Individual Risk *Information concerning the reconciliation of Non-GAAP measures and cautionary

information with respect to the 2009 projections can be found at the beginning of this presentation. (1) 2009 projected premiums are managed catastrophe premiums up 15%, Individual Risk

premiums are flat, and Specialty reinsurance premiums up 20%. These estimates were originally disclosed on the Companys February 12, 2009 earnings call for the quarter and year ended December 31, 2008. Gross Written Premium |

11 Reinsurance: Leveraging off of our market leading franchise Exposure based pricing that meets our portfolio return hurdles Quick response Customized products Capacity for large lines Advice on cat risk management Superior credit quality and willingness to pay Normal open market position Plus preferred signings on open market transactions Plus private market transactions Option to renew business written for fully collateralized vehicles RNR delivers value RNR gets preferred status |

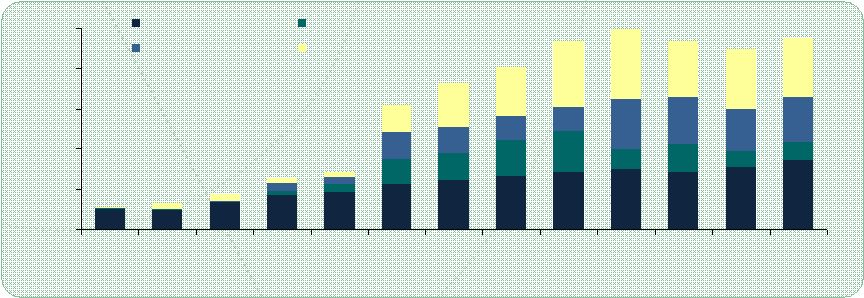

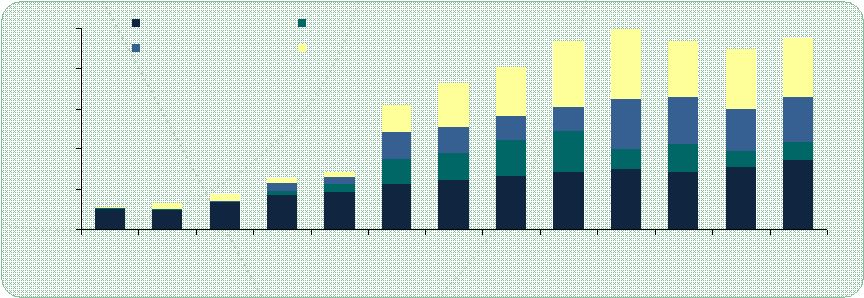

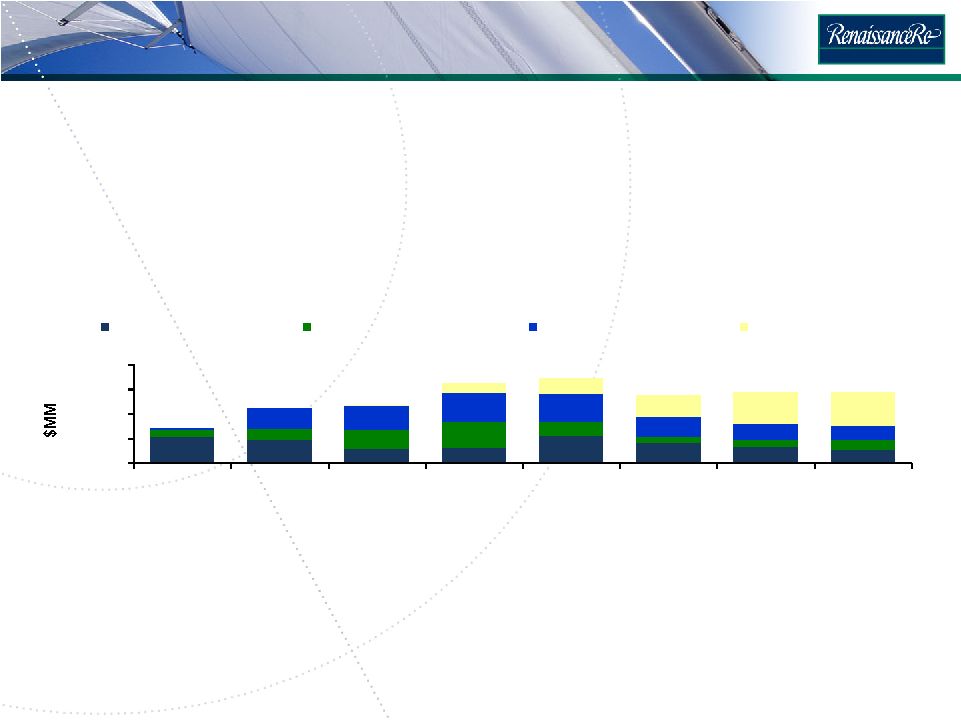

12 Discipline requires knowing when to grow and when to shrink Market conditions matter we decrease when conditions soften (e.g. late 1990s and 2008), and grow when pricing improves (e.g. 2002) Specialty premium can be lumpy due to our willingness to participate on large

lines; we remain disciplined in a more competitive market 0 500 1000 1500 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 (proj. 1) Specialty Managed Cat ceded to fully-collateralized J.V.'s* Managed Cat* *Information concerning the reconciliation of Non-GAAP measures and cautionary

information with respect to the 2009 projections can be found at the beginning of this presentation. (1) 2009 projected premiums are managed catastrophe premiums up 15% and Specialty reinsurance premiums up 20%. These estimates were originally disclosed on the Companys February 12, 2009 earnings call for the quarter and year ended December 31, 2008. Managed Catastrophe and Specialty Premiums |

13 Individual Risk: Building out our platform Our focus is on high margin primary insurance and quota share reinsurance We partner with other insurance companies and program managers (intermediaries) who source the risk and provide back office support We target a small number of partners with the following characteristics: Leaders in their classes of risk Large premium volume Efficient back offices Focused on data, systems and rigorous risk analytics We are developing proprietary risk modeling tools to track and evaluate exposures

|

14 14 Market conditions dictate writings we will decrease when conditions soften and grow when pricing improves Individual Risk Premiums (1) 2009 projected Individual Risk premiums are flat. These estimates were originally

disclosed on the Companys February 12, 2009 earnings call for the quarter

and year ended December 31, 2008. 0 200 400 600 800 2002 2003 2004 2005 2006 2007 2008 2009 (proj. 1) $MM Commercial Property Personal Lines Property Commercial Multi -line Multi Peril Crop |

Extending into attractive markets and expanding our operational capabilities 15 Agro National Claims Management Services Agro National: a managing general underwriter of crop insurance We partnered with Agro National over the past four years to write multi-peril crop insurance policies Acquisition provides means to expand in growing agricultural market CMS: a privately-held provider of claims administration, adjustment and consulting services Provided third party administrative services to our subsidiaries on an outsourced basis since 2005 CMS has important operational capabilities and gives us greater control of a core function key to our plans for U.S. growth |

Renaissance Investment Managers (R.I.M.) Ventures: Leveraging and expanding our franchise 16 Joint Ventures (J.V.) permanent vehicles that augment RenRes offering to clients and brokers Top Layer Re & DaVinci Re Packaging & Selling limited-life vehicles to provide incremental capital to clients and brokers including side cars and cat bonds, Starbound I (2006) & II (2007). Timicuan Re (2006) Venture Capital capital solutions to clients as well as strategic investing Tower Hill, Platinum warrants risk mitigation services/products to the natural gas, heating oil, and energy industry; also includes trading of weather derivatives Weather Predict Consulting (W.P.C.) weather forecasting, modeling, advisory services and outreach in support of RenRes businesses WindX, Wall of Wind |

Hurricane Science: Extending our scientific leadership through our current hurricane risk mitigation efforts StormStruck The Hurricane Risk Mitigation Leadership Forum series The RenaissanceRe Wall of Wind 17 |

18 Financial Profile: Strong capital and liquidity position, our balance sheet and capital base remain strong $0 $1 $2 $3 $4 $5 $6 Common Preferred Funded debt Undrawn debt JV capital* * excluding $3.9 billion of capacity at Top Layer Re **Reflects the redemption of ~$250 million of preference shares and funded debt, which were redeemed during Q1 2007

|

19 RenaissanceRe is well-positioned Balance sheet and capital base are strong, we are focused on managing our assets optimally Our organization is strengthened by new talent, widening our breadth of expertise Our distinctive corporate culture remains a key competitive advantage We continue to strengthen our position as a leader in property cat reinsurance

with superior risk analytics We view ourselves as a capital provider to our clients and provide capital principally in the form of reinsurance, alternative forms of capital are provided

to meet clients evolving needs We are well positioned to continue to serve our customers in timely, innovative ways, to seize attractive opportunities when they arise and to build

shareholder value in the years ahead |

RenaissanceRe Holdings Ltd. Renaissance House 820 East Broadway Pembroke, HM 19 Bermuda Tel: (441) 295-4513 www.renre.com |